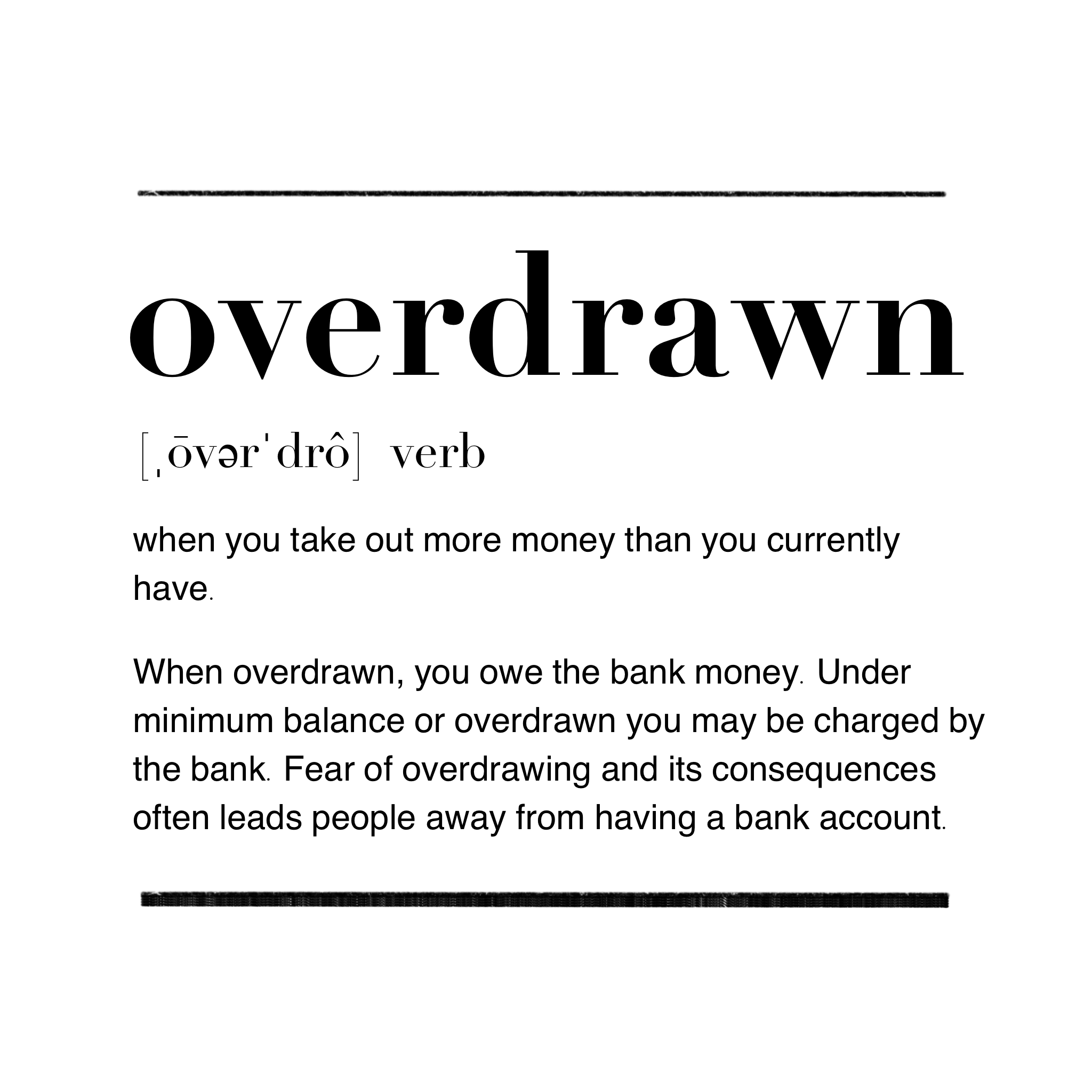

What’s the cost of being unbanked?

Have you ever heard the phrase: “It’s expensive to be poor?” Well, that term definitely applies here too.

When using alternative banking choices, it costs money to cash in checks, and payday loans can potentially cost extremely high interest fees.

A payday loan is a loan people normally take from non-bank lenders for normally around $500 and is supposed to be paid back by the next paycheck. However, one can extend the due date of when to return the money with around a $20 fee.

As for sending money overseas, wiring costs can go up to $50, although if using a bank, there is a set cost for each bank of around $15, or at most $45, for it to be sent.

Some working class people are paid “on credit card,” meaning they have a plastic card that has all of their wages, not a bank account. While this might be good temporarily, if you lose or have the single card stolen, that’s all your money gone with a poof!

With money outside of a bank account floating around either in cash or card, it has a higher risk of being lost and unprotected.

It costs much more to be unbanked.

When you’re underage, you can have a bank account under your parents name until you turn 18. Once you meet age requirements, the account becomes yours and parents no longer have access to it.

Having a bank account provides:

- Preparation for work, school, friends and the future.

- Paypal, Venmo and Cash App accounts may not need a bank account, but to put in money, one has to enter their debit or credit card number.

- As for jobs, whether it’s part-time or full, they normally need a checking account or something else they can access for payment. It makes business transactions easier between parties, as someone may not always be accepting of alternative payment.

- Protection

- Federal laws protect your money from fraud, theft and safety in case of a disaster.

- For example, you get an account with Bank of America. One day everything blows up: your wallet, your house and your local bank. If you go to another Bank of America, they will be able to help you retrieve your money. It’s like insurance without all the extra steps.

- The whole point of my parents’ exercises when I was little was to teach me about saving money. While I could’ve learned that without a savings account, I would have money lying around that could beー once againー stolen or destroyed. Then I would’ve saved nothing.

- Easier access

- When you cash in your checks or communicate with others for loans, they may not always be available or one may not always have access to these services. While banks are not open 24/7 either, they have consistent schedules and immediate access through card or direct deposits through payment. Through direct transfer, it’s faster and safer.

- FUN FACT: The bank can’t deport you.

- Students or people who are still undocumented, I hope you are reassured if this was a fear.

- For most banks, when you open a bank account, you typically need a Social Security Number or an Individual Taxpayer Identification Number. If one doesn’t have an ITIN or SSN, they can apply for one via the IRS.

- Here is a list of banks that allows one to open a bank account without a SSN, although some banks may ask for further identification, like passports, photo IDs, or an address. For more information about deportation, you can visit usa.gov.

Your donation will support the student journalists of Bellaire High School. Your contribution will allow us to purchase equipment and cover our annual website hosting costs.

Joy Xia • Dec 20, 2023 at 9:55 am

I really like this topic. Thank you for addressing it!

Kate Steinbach • Nov 7, 2023 at 12:25 am

Great story! I thought that this was very informative!